January 15, 2026

MACROECONOMIC HIGHLIGHTS

Positive:

- Q3 QDP gains further momentum (+4.3%) and clocks in at best pace since summer ‘23 with Consumption +3.5% while business investment keeps trending higher despite uncertainties

- Inflation slows back down through November amid softer Shelter & Food, helping y-o-y ease back to 2.7% (core 2.6% slowest in ~5 years)

- Housing gains some more traction as rates plumb YTD lows: existing sales inch up through early winter with 1st time buyers rising, while average home prices up only ~1% y-o-y following spring slowdown

Negative:

- Hiring slows down dramatically after -100K (gov’t) layoffs in October, while jobless rate worsens to 4.6% (a four-year high)

- Consumer Sentiment ends December down 5th straight month amid gloomier Present business condition readings, while Expectations below the ‘recessionary level’ almost a year running

- Manufacturing stuck in first gear: industrial production ticks up 3rd time in 4 months but annual change mild (+2%) and manufacturing payrolls shedding since April;

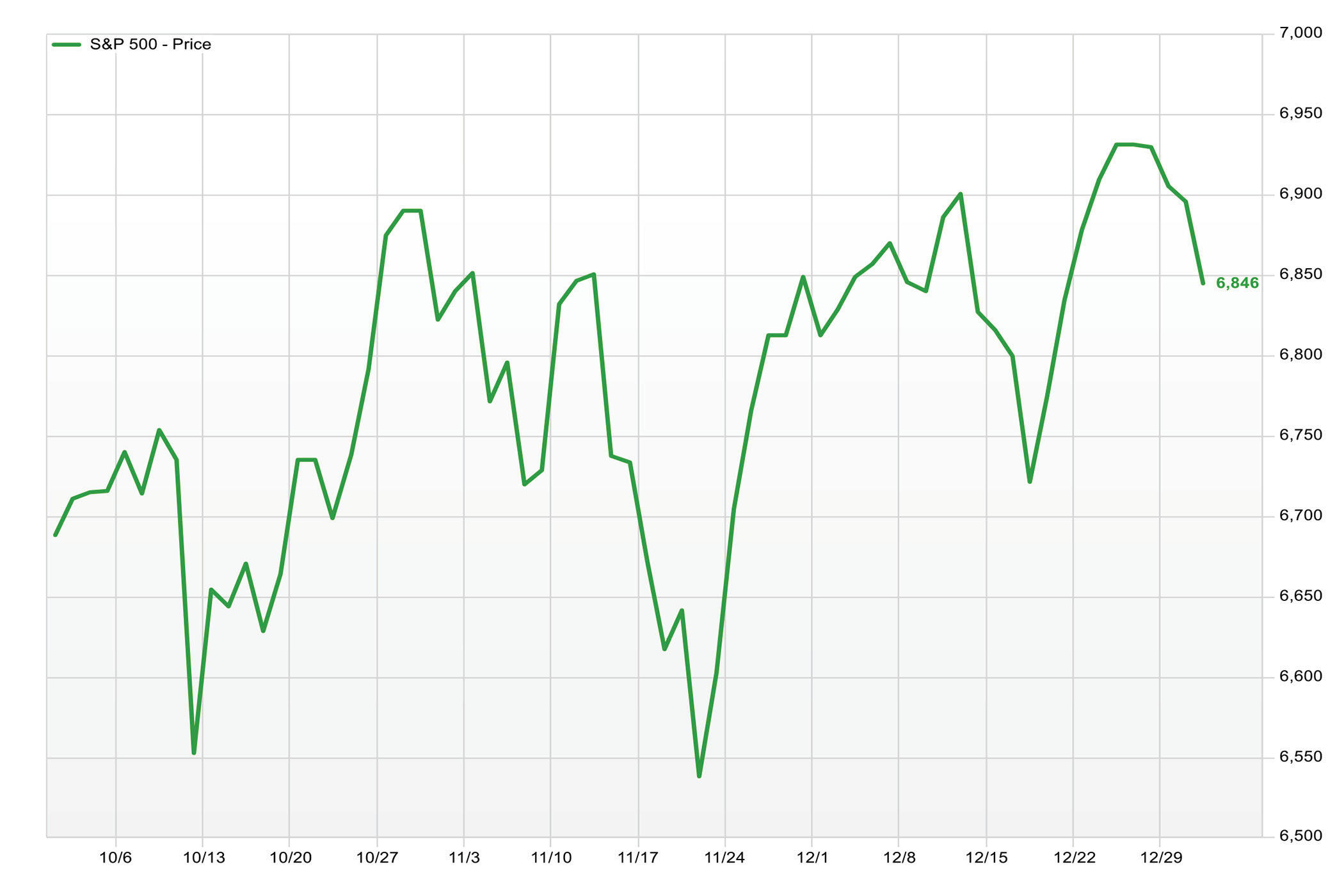

S&P 500 Performance:

Finishes up 3rd straight quarter after a choppy November, led by Healthcare (+12%) and Communications (8%), but safe-haven Real Estate and Utes -1%

S&P 500 Earnings:

Third quarter earnings came in nicely ahead of consensus, with well over 80% beating expectations–the best since the early virus recovery days. Also, profits were up a similar low-teens percent again (14%), with sales growth also the best in a few years (+8%). Tech and Utilities led (as expected) with +20% earnings growth, but the former would be ~17% if the semiconductor names were excluded, while NRG Energy greatly aided the latter. Excluding such, Financials were the sole sector with a +20% bottom-line improvement. ‘The “Magnificent 7” witnessed profit growth slow from upwards of 30% to ‘only’ about 18%, although investors expect a pickup moving into next year. Lastly, investors anticipate growth will moderate to 8% this quarter vs. a tougher 18% comparison, but still cap a 12% full year expansion with the ‘Mag7’ outpacing (+22%).

Notable Developments:

- China GDP slows again (to +4.8%) despite an easier year ago comparison, but YTD expansion is running a tad above the 5% goal, as production heats back up (6.5%)

- U.S. announces new Russian sanctions (Lukoil and Rosneft) in an effort to isolate them and curb oil revenue being used for war, while EU moves to ban their LNG starting ‘26

- Fed cuts rates a consecutive meeting (¼pt to 4% and lowest in a few years), in an effort to cushion the slower labor market despite lack of economic data during shutdown

- U.S. to halve Chinese tariffs (to 10%) in exchange for a reduction in chemicals made to create fentanyl, as well as tempered export controls on rare earth metals

- ECB holds target rate steady a 3rd straight meeting (at 2%) as inflation hovers just above their 2% target

- Senate ends longest government shutdown ever, which funds operations through January, but also funds Agriculture Dept, military & legislative branch a full year

- Trump relaxes tariffs on over 100 agriculture and food products, including beef, coffee, fruit, etc. in an effort to address consumers’ cost of living concerns

- Fed cuts rate third straight meeting (¼pt to 3.75%), while Chair Powell noting job growth likely weaker-than-reported, but projections point to only 1 more cut in ‘26

- Japan raises rate (¼pt to 0.75% and highest in three decades) after being on hold nearly a year, which could cause capital to flow back into country (and away from U.S. assets)

Corporate Activity:

- Novo Nordisk buys Akero Therapeutics ($5.2B) which has a MASH drug pending approval, but loses to Pfizer in deal for Metsera ($10B), while Abbot buys Exact Sciences ($21B)

- Kimberly-Clark acquires (J&J spinoff) Kenvue ($40B), while Netflix wins bid for Warner Bros. assets ($72B) once they get split from the cable networks

Disclosure

The information and opinions provided herein are provided as general market commentary only and are subject to change at any time without notice.

This commentary may contain forward-looking statements that are subject to various risks and uncertainties. None of the events or outcomes mentioned here may come to pass, and actual results may differ materially from those expressed or implied in these statements. No mention of a particular security, index, or other instrument in this report constitutes a recommendation to buy, sell, or hold that or any other security, nor does it constitute an opinion on the suitability of any security or index. The report is strictly an informational publication and has been prepared without regard to the particular investments and circumstances of the recipient.

Past performance does not guarantee or indicate future results. Any index performance mentioned is for illustrative purposes only and does not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Index performance does not represent the actual performance that would be achieved by investing in a fund.